Revolving loan funds are a key tool for business district revitalization. They can provide crucial gap financing, especially when the investment doesn’t meet the equity requirements of commercial financing or when a lower interest rate is needed to make the project work. Those conditions apply to a good percentage of start-up businesses and projects involving historic properties.

Many localities and economic development authorities have resources for offering revolving loan funds, originally funded through sources like the Community Development Block Grant (CDBG) program at DHCD or the Revolving Loan Fund Program at USDA Rural Development.

These grants allow communities and allied community-based nonprofits to make loans to businesses in the community at very low rates, with program staff acting as fund administrator and a volunteer board or team acting as the loan committee. Communities across the commonwealth have used revolving loan funds to support the development and growth of local businesses that are creating rural jobs, and they’ve learned lessons and best practices along the way.

In Floyd, Virginia, Community and Economic Development Director Lydeana Martin oversees the revolving loan fund, which began ten years ago with a $100,000 grant from USDA Rural Development. “We called it the “Floyd 5 & 10″ because we made loans of $5,000 or $10,000 for a term of 5 or 10 years,” says Martin. “We wanted it to feel approachable for a broad range of people, whether they were looking to provide services like childcare or start small scale construction or production firms.”

The County has indeed seen a wide array of businesses, ranging from technology to niche food production. Many businesses, such as restaurants, food trucks, retail shops, an independent pharmacy, and wellness companies, are geared for location in commercial districts such as the town of Floyd’s, which is clustered around the county’s sole stoplight/

“We’ve loaned all $225,000 from Rural Development in 22 loans,” says Martin, “and we are now loaning the money that has cycled back in repaid loans.”

Martin hopes to join the Wytheville conversation. She has a number of lessons learned to share, and has some questions herself. For instance are communities doing their own loan closings and liens. “Getting to closing after everything else is approved is the most time consuming and frustrating aspect,” says Martin. “It often takes four to six weeks, and we’d like to shorten that.”

Other communities have questions as well. While many have access to funds, some struggle in deploying them efficiently and effectively. Virginia Community Capital, USDA Rural Development, and Virginia Department of Housing and Community Development hopes to create a forum for conversation and knowledge sharing around the tool.

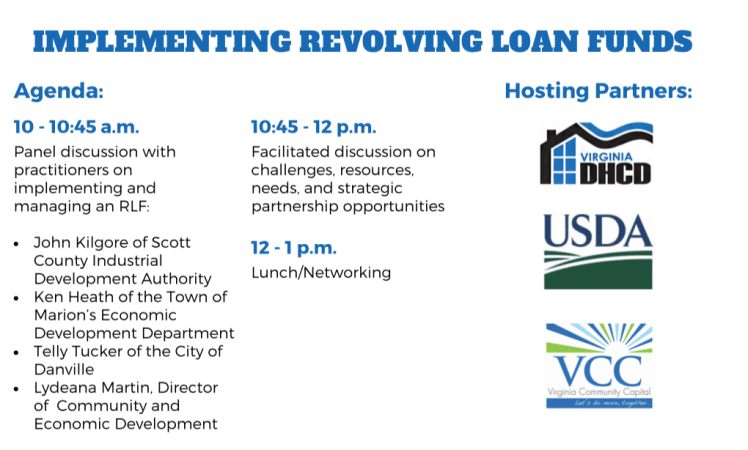

“Implementing Revolving Loan Funds” is a half-day facilitated conversation taking place around the commonwealth over the coming year. Attendees will discuss successes and challenges in using revolving loan fund strategies in building the business community’s capacity. It’s recommended for communities running a loan program or just interested in exploring the idea.

Expect to hear best practices around earning trust from businesses, taking the long view, preparing for loan defaults, shaping a loan committee, scaling up for second-stage loans, tracking borrowers, and, of course, funding programs.

There will be three opportunities to attend. The first will take place on August 21, 2019 at the VHDA offices at 105 E. Main Street in Wytheville. In subsequent months, gatherings will take place in the Shenandoah Valley and on the eastern side of the state. While dates aren’t set, submit your contact information at the bottom of the page and you’ll be added to the list.

The panel and facilitated conversation will be followed by a networking lunch.

- Register for the Wytheville event.

- Download the flyer to share.

- Add the Facebook event to you calendar.

SIGN UP FOR FUTURE EVENTS: